Tax Data Analytics - How data analytics can add value using the example of a global transfer pricing documentation project

Key Facts

Targeted analyses of tax data help you uncovering potential tax risks and tax opportunities

Unfortunately, the potential that your data may offer is often wasted - either because required BI tools are not in use or the potential is simply not recognized

Everyone talks about data & analytics („D&A“). All tax experts dream of automated analyses of tax data at the push of a button in order to meet compliance requirements and leverage optimization potential. After all, a targeted evaluation of tax data provides valuable insights and risks can be uncovered and proactively managed. However, the potential of tax data analyses is often underestimated because either available analysis capabilities are overlooked or required BI tools are simply not in use yet.

With the following use case, we show you how the data collected as part of a global transfer pricing documentation project cannot only be used for their immediately intended purpose - the preparation of the Local Files - but also to uncover tax risks and opportunities by using D&A tools.

In almost all countries, companies must prepare a transfer pricing documentation - so called Local Files - in order to meet transfer pricing compliance requirements. The basis for the creation of the Local Files is transaction-specific information such as transaction volumes per company, transaction party, transaction group and, if applicable, transaction-specific margins in the period to be documented. More often than not, such information is put aside after completion of the documentation project and not analyzed further. In doing so, taxpayers waste a lot of potential which targeted data analytics would otherwise offer.

Low-code solutions such as Alteryx are ideal for such data analytic tasks. Such solutions are flexible to use, user-friendly and can be run as often as required at the push of a button. The results can then be graphically illustrated using visualization tools such as PowerBI or Tableau to make the key information and insights easily accessible for a wide range of recipients.

The following provides some examples for such analyses and the offered benefits.

1. Increase transparency

A transparent visualization of the transaction values per transaction group, of the transaction flows between the transaction parties and of the amounts spent and received per group company, as depicted here, helps setting priorities when preparing the Local File. At this stage, potential inconsistencies already become transparent, e.g. transactions between companies that contradict the business purpose or the functional profile of the companies.

2. Uncover mismatches

If transactional data is collected decentrally, inconsistencies can quickly arise if Company A reports a transaction with Company B, which Company B in turn does not report (total mismatch) or at significantly different amounts (partial mismatch). Such inconsistencies may arise e.g. due to timing discrepancies when recording the transactions or due to exchange rate effects. Very often, however, they are simply the result of an incorrect mapping of journal entries to transaction groups.

The absolute value of mismatches and the number of transactions with mismatches provide insights about the extent of the inconsistencies and the need for action to review existing processes and, where necessary, optimize them. The breakdown of mismatches into transaction groups and by reporting or receiving company, as shown in the dashboard, helps narrowing down the problem and quickly identifying the largest risk items. Recommended focus areas for efficient approaches to solve the problem can be derived through cluster analyses, e.g. by showing out companies that have high absolute amounts with a simultaneously low count of mismatches.

In practice, such inconsistencies often account for a large proportion of documented transactions. In times of increasing exchange of information between tax authorities, such inconsistencies present potential risk positions which, in a worst case scenario, may cast doubt on the compliance with proper accounting principles during a tax audit. Unfortunately, many companies are discouraged by the alleged complexity of these analyses and underestimate their risk positions as they lack the relevant insights.

3. Monitor margins & risks

In order to demonstrate the arm's length nature of transfer prices, transaction-specific margins are often determined and compared with ranges of margins identified in benchmark studies. Companies with an entrepreneurial role in transactions require information on the margins of their respective transaction partners in order to prove the arm's length nature of their transactions. With the help of this information, the entrepreneur can demonstrate that the routine business has not generated an unreasonably high profit and that the entrepreneur behaved in compliance with the arm's length principle.

This is not merely (but also) an issue of data availability. If routine companies earn "too little" or "too much" compared to the benchmark results, this translates into a tax risk domestically or abroad, respectively. The respective tax authorities could request an income adjustment at least to the outer edge of the range of benchmark results with the corresponding tax consequences.

BI tools support the preparation of margin analyses and ongoing risk assessments for any number of data points, which can be visualized in dashboards, as illustrated here. The aggregate value of potential unilateral adjustments provides information on the overall risk position of the group. Multiplying the potential amount of adjustments by the respective tax rate of the country gives a risk indication on the tax effect of potential tax authority adjustments. A breakdown of potential adjustments by transaction group and company helps to identify the main risk positions and the greatest need for action.

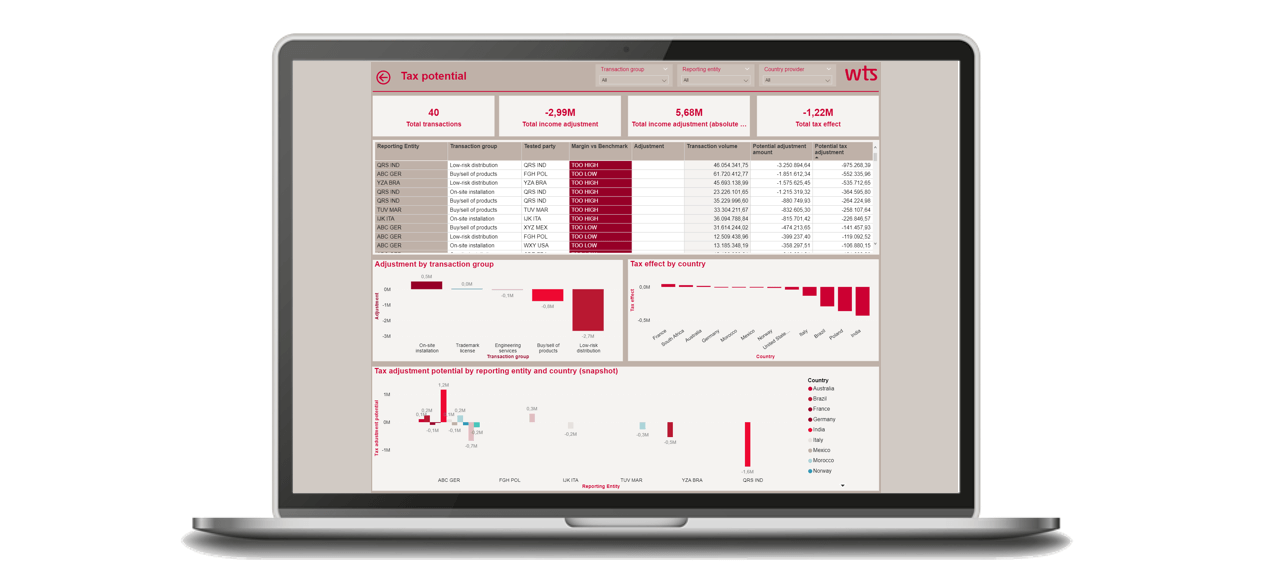

4. Identify tax potential

The available information on company margins gives insights about a group’s risk position, but can also be used to analyze whether tax potential could be exploited through a proactive operational transfer pricing management. It is assumed that transfer price adjustments are possible to steer the operating margins of routine companies to a value that always lies within the range of the benchmark results to ensure arm's length outcomes. The tax potential is simulated in a variable model based on a bilateral income adjustment for both the entrepreneur and the routine companies and calculation of the resulting tax effect.

In the example presented here, an adjustment to the median is simulated. In total, the group can improve its tax position compared to the baseline scenario, where the group did not engage in any proactive transfer pricing management, and reduce the tax amount while at the same time increasing compliance. The dashboard shows the adjustments per transaction group and reporting company as well as the tax effect per reporting company, broken down by the respective countries.

Conclusion

Tax data analytics can offer great advantages to companies in terms of increasing their compliance and uncovering tax potential. A lot of relevant data is already available for existing compliance requirements, which can be used to increase transparency and provide actionable insights to mitigate risks and leverage tax potential through targeted data analytics. Where this potential remains undetected, companies may actually waste money. With the targeted use of flexible low-code solutions, tax departments can analyze large amounts of data at the push of a button and create insightful visualizations in dashboards, independently of information required to be contributed by other parts of the organization such as controlling or the IT department.

We look forward to help you with this. Reach out to us!